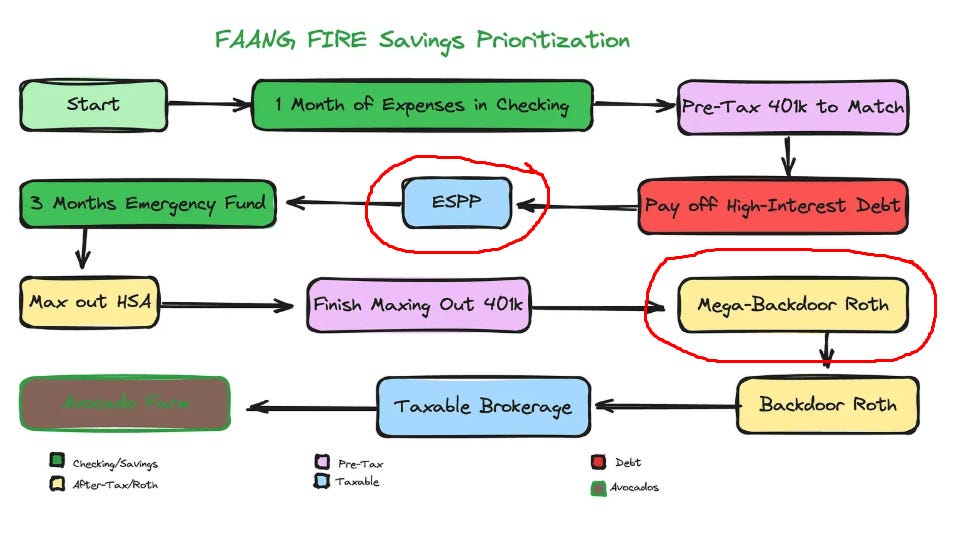

ESPP vs. Mega Backdoor Roth: The Problem With “Always Take the Free Money”

Families with high incomes and disciplined spending should ideally leverage every available wealth-building tool from 401(k) matching and ESPPs to tax-advantaged accounts like the Roth 401(k) and Roth IRA. However, cash flow constraints often force a choice. Because strategies like the ESPP and Mega Backdoor Roth require direct payroll deductions, a limited paycheck or competing financial priorities may make it impossible to maximize both. In these cases, families need to choose a strategy they want to prioritize.

Online guides including FAANGFire often suggest prioritizing ESPP arguing that it’s basically free money. But does the greedy algorithm always work when we plan our contributions?

The Hidden Cost of ESPP

The problem with the Employee Stock Purchase Plan (ESPP) is that while it may look like “free money,” it can distract from a more impactful tax strategy: the Mega Backdoor Roth.

People who prioritize ESPP over the mega backdoor may be missing two key points:

If they sell the stock without waiting two years from the grant date, the gain is taxed as ordinary income.

The proceeds often end up in taxable brokerage accounts, where future gains are also taxed.

In reality, the decision between ESPP and the mega backdoor depends on a family’s needs. If they don’t need access to the money anytime soon, focusing on the mega backdoor and ignoring ESPP might be a better strategy if they can’t afford to do both.

Consider this example:

Family lives in California

Household income is $600K

Marginal ordinary income tax = 44.3% (federal 35%, CA 9.3%)

Marginal capital gain tax = 33.10% (federal 20%, CA 9.3%, NIIT 3.8%)

Employer offers 15% ESPP discount

Employer offers a 401(k) plan with mega backdoor support

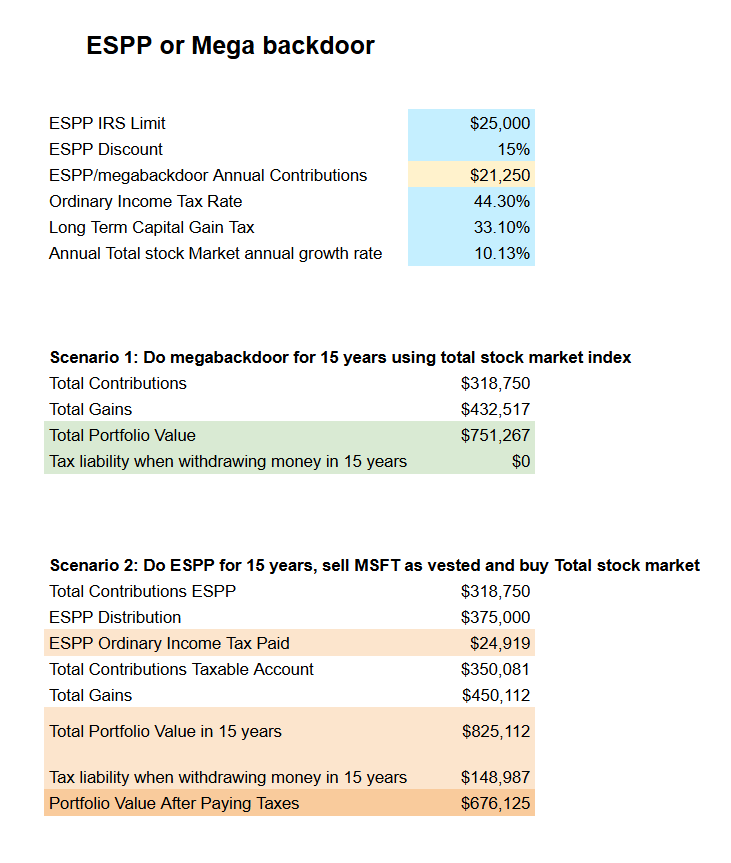

To make two scenarios comparable, we assume that the family can allocate only $21,250/year from their paycheck and must choose between ESPP and the mega backdoor. Here’s how the numbers work out over 15 years:

Scenario 1: Do Mega Backdoor for 15 years using total stock market index

Total contributions over 15 years = $318,750

Total gains after 15 years = $432,517

Taxable gains = $0

Total portfolio value = $751,267

Scenario 2: Do ESPP for 15 years, sell ESPP as it vests and buy Total stock market

Total Contributions into ESPP = $318,750

ESPP Distribution = $375,000

Contributions into taxable account (after tax) = $350,081

Total gains after 15 years = $450,112

Capital Gain tax paid when withdrawing money = $148,987

Total value after tax = $676,125

Mega backdoor comes out ahead for this family if they don’t need short-term liquidity:

Higher portfolio value: $751K vs $676K

Money ends up in a tax-free vs taxable account

Less hustle: No need to sell ESPP and buy VTI every vest

Now let’s imagine, the family doesn’t need to sell the assets and use the money immediately after 15 years. They quit their jobs but keep the money invested without touching for another 15 years.

Scenario 1: Mega Backdoor portfolio

Total portfolio value at year 15 = $751,267

Cost Basis = N/A

Growth Rate = 10.13%

Total portfolio value at year 30 = $3,194,323

Scenario 2: ESPP Portfolio in Taxable Account

Total portfolio value at year 15 = $825,112

Cost Basis = $375,000

Growth Rate = 10.13%

Total portfolio value at year 30 = $3,508,306

Capital Gain tax paid when withdrawing money = $1,037,124

Total value after tax = $2,096,181

The difference between the two scenarios would be $3.1M - $2M = $1.1M after tax

Look Back Provision Changes The Math

The previous comparison assumes a flat 15% discount on the current stock price. However, most top-tier ESPP plans include a “Look-back” provision. This allows you to purchase the stock at a discount of either the price at the beginning of the offering period or the end, whichever is lower. In a rising market, this isn’t just a 15% gain, it can be a 50% or even 100% gain in a single six-month window.

Among top companies, only Microsoft doesn’t have a “Look-back” provision.

How can it be Mitigated

The “paycheck squeeze” is the primary barrier preventing families from maximizing both strategies simultaneously. Once you understand the potential challenges and long-term effects of different strategies on your wealth, you can build a more effective plan.

If your base salary cannot support the combined deductions for both a maximum ESPP and a Mega Backdoor Roth contribution, you have a few options:

Pick one strategy that benefits your family the most. For some families it would be ESPP, for others it might be a mega backdoor. Understanding long-term trade-offs can help you make a better decision and avoid local optimums when building your wealth. This is the simplest approach.

Use the “ESPP Carousel”. ESPP is a liquid asset that can be used 6 months later to cover living expenses. Once the first ESPP period vests, sell the shares immediately. Use those proceeds to supplement your next six months of suppressed paychecks. The biggest hurdle is the initial 6-month accumulation period where your take-home pay is significantly reduced.

401k Bonus Front-Loading. Many FAANG-style companies allow you to set a separate, higher contribution percentage for your annual or sign-on bonuses. You can direct your performance bonus toward your 401(k) and Mega Backdoor Roth. By hitting your limits early in the year, you free up your remaining paychecks to focus entirely on ESPP.

Use RSU to cover living expenses. If you receive Restricted Stock Units, instead of thinking of them as your savings, you can treat them as a “paycheck supplement.” This allows you to “teleport” your RSU value into a tax-free Roth environment.

Conclusion

An ESPP is a great benefit, but if you find yourself in a situation where you need to choose between an ESPP and a Mega Backdoor Roth, you should be aware of the long-term benefits of the Mega Backdoor Roth. The ‘Greedy Algorithm’ sometimes fails when it optimizes for an immediate 15% gain while ignoring the decades of tax-free compounding offered by a Mega Backdoor Roth.

P.S. If you want to explore these trade-offs using your own inputs, tools like Nauma are designed to help you build and stress-test different scenarios.

For those who want help going deeper, we also work with a small number of clients to build custom models tailored to their career, family, and risk profile. We currently have limited availability in May and June. Details are here.