Financial Planning for Families With Special Needs

Coordinating public benefits, trust taxation, and legal protections for a family’s lifelong plan

Financial planning is complex for any family. To create a plan a family can rely on, they need to understand how inflation, investment returns, taxes, and future income and expenses may affect their finances. Families with special needs face an additional challenge: their assets often need to support at least two major goals: the parents’ retirement and their child’s needs for the rest of the child’s life.

Families must plan for both goals while navigating complex government benefit programs, tax considerations, asset protection, and estate planning. While raising a typically developing child in California may cost between $400K and $800K, depending on the family’s preferences, the cost of raising a child with special needs may range from $1M to $2.4M, depending on the level of support required.

On top of that, raising a child with special needs requires extraordinary effort, patience, and love. Parents in these families often need to work much harder to keep everything running. When they also need to create financial and estate plans, they can quickly become overwhelmed by the complexity.

Complexity

We have been working with families raising children with special needs and have witnessed firsthand both the challenges they face and the complexity they need to navigate.

To secure their child’s future, families often rely on public benefits such as Supplemental Security Income (SSI) and Medicaid, known as Medi-Cal in California. These programs provide support and health insurance but are governed by strict eligibility rules that frequently change.

For SSI, an individual generally cannot have more than $2,000 in countable assets.

California Medi-Cal asset limit is $130K in 2026, with a planned reduction to $21K in 2027. Income generally must remain below 138% of the federal poverty level (FPL), or about $1,836 per month.

To navigate these restrictions, families need to coordinate their savings and use specialized tools: ABLE accounts and third-party special needs trusts (SNTs).

A third-party SNT is a common way to hold family wealth after the parents’ deaths while preserving the beneficiary’s eligibility for public benefits. However, it also creates tax-planning complexity. Non-grantor trusts are subject to compressed tax brackets. While an individual does not reach the 37% federal tax bracket until taxable income exceeds approximately $640K, an irrevocable non-grantor trust reaches the same bracket at approximately $16K.

Creating trusts to protect assets and preserve eligibility for public benefits requires each family to become the author of its own family constitution.

Whether they want to or not, families often need to learn many estate-planning terms and determine how to establish proper checks and balances in their trusts to prevent unwanted trust takeovers by beneficiaries, as well as abuse and poor governance when professional private fiduciaries (PPFs) are involved.

These are not easy tasks for a family that needs to work hard just to keep up.

Thoughts on Navigating the Complexity

I’ve recently been involved in reviewing and analyzing various trust documents for clients, including irrevocable non-grantor special needs trusts (SNTs), dynasty trusts, and revocable living trusts (RLTs). I’ve also participated in meetings with estate attorneys to discuss these documents and their provisions.

Estate planning is one of the most complex legal disciplines, and attorneys spend many years developing expertise in this area. That said, a willingness to learn, the time spent carefully reading legal documents, and common sense can take us surprisingly far.

I’ve put together some thoughts and observations based on my ongoing experience in this space.

1. Financial Planning Before Estate Planning

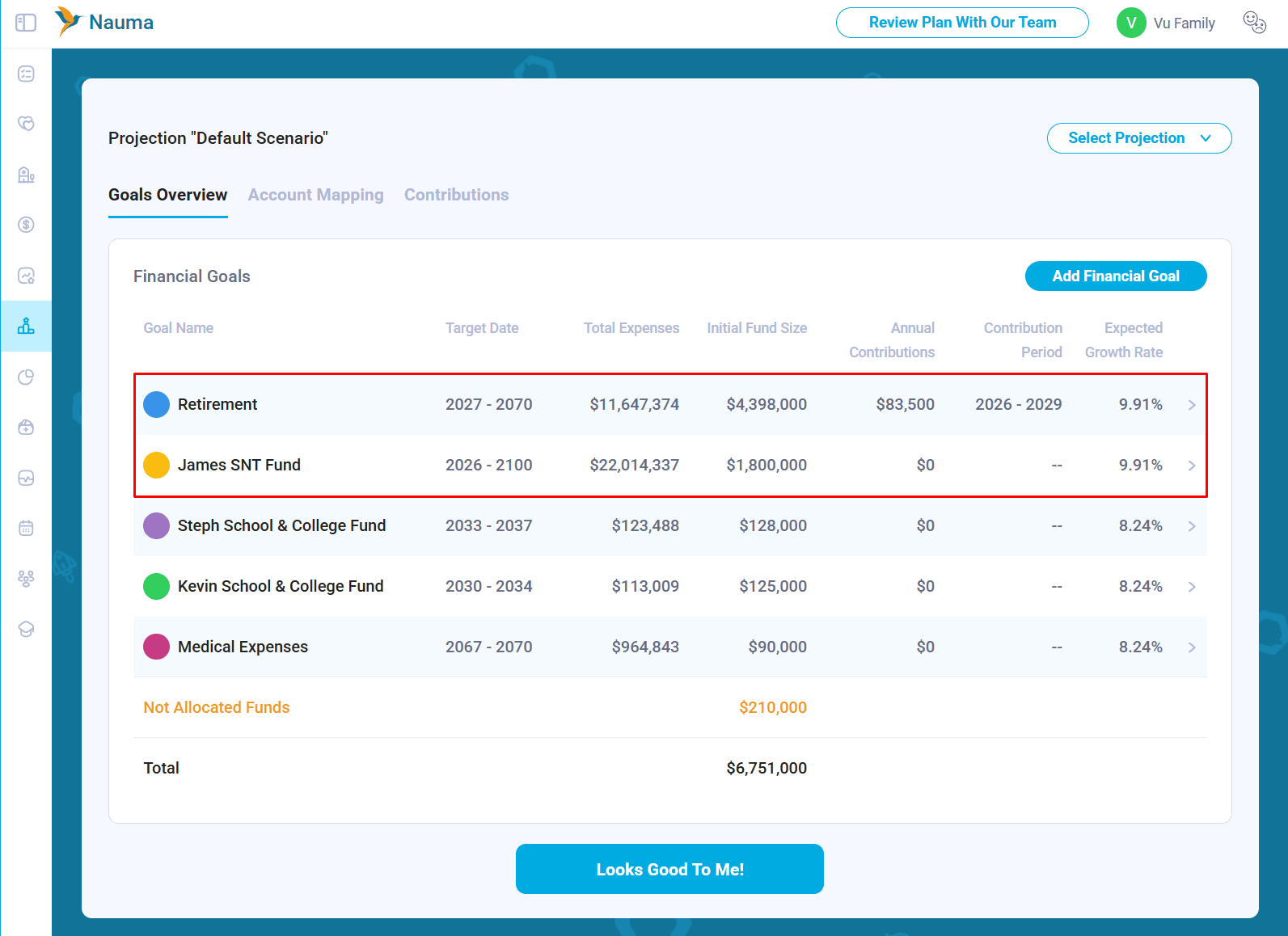

Attorneys typically have limited time to spend with each client, and their hourly rates are high. It is therefore helpful to have an up-to-date family financial plan and projection available before beginning the estate planning process. This information can help the estate attorney tailor the documents to the family’s circumstances and avoid unnecessary complexity that may cost the family additional time and money in the future.

When an estate attorney does not have a clear picture of how the family’s finances may change over time, it can be difficult to decide which provisions are necessary in the estate plan. For example, the family’s projected estate size can help determine whether the plan should include estate-tax or generation-skipping transfer tax provisions, such as exemption allocation, a bypass trust, or continuing trusts for descendants. Whether these provisions are appropriate depends on the family’s projected assets, beneficiaries, and broader circumstances.

Another example is having the RLT become irrevocable upon the first death, sometimes referred to as an administrative trust, followed by the transfer of assets into a new revocable living trust for the surviving spouse. This structure is often used in blended families to protect the interests of children from prior marriages. Whether an administrative trust is necessary depends on the family’s circumstances, but it can require additional work to retitle assets when inheritances are distributed and assets are transferred from the administrative trust to the surviving spouse’s new RLT.

Some families may also have substantial savings in tax-deferred accounts. Understanding how these accounts are expected to change over time can help the family plan transfers to irrevocable trusts while reducing the impact of compressed trust tax brackets. For example, the estate plan can direct taxable and tax-deferred accounts to different beneficiaries based on their tax situation. Without this information, an estate attorney may default to an equal distribution among the children without fully considering the tax implications.

2. Keeping Documents In Sync

A fairly common situation is that a family first creates a simple revocable living trust, often through a service provided by an employer, and then hires another attorney a few years later to establish a third-party SNT or a dynasty trust.

Surprisingly, the RLT documents are not always reviewed and updated to reflect the family’s changing needs or the creation of new trusts. In some cases, estate attorneys decline to update documents drafted by another attorney. There are two common reasons for this:

Liability: If Attorney B changes a trust created by Attorney A, Attorney B may take on some responsibility for the entire document. If the original trust contains a serious mistake, Attorney B could still be pulled into a future lawsuit.

Efficiency: Reviewing and understanding another attorney’s documents can take more time, and cost the client more, than creating new documents from scratch.

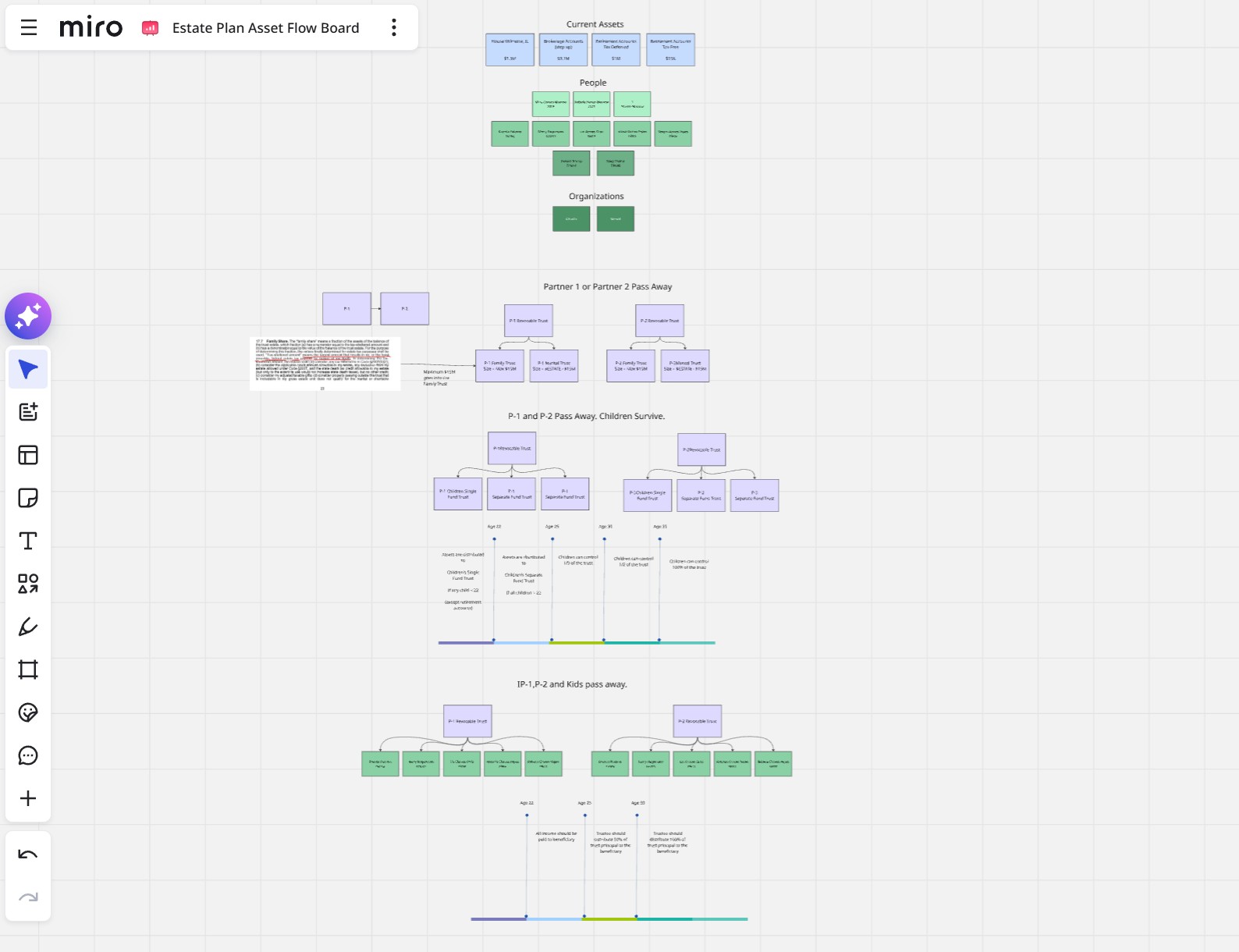

One effective way to identify these issues is to create an asset flowchart based on the legal documents and verify that the assets will move as intended.

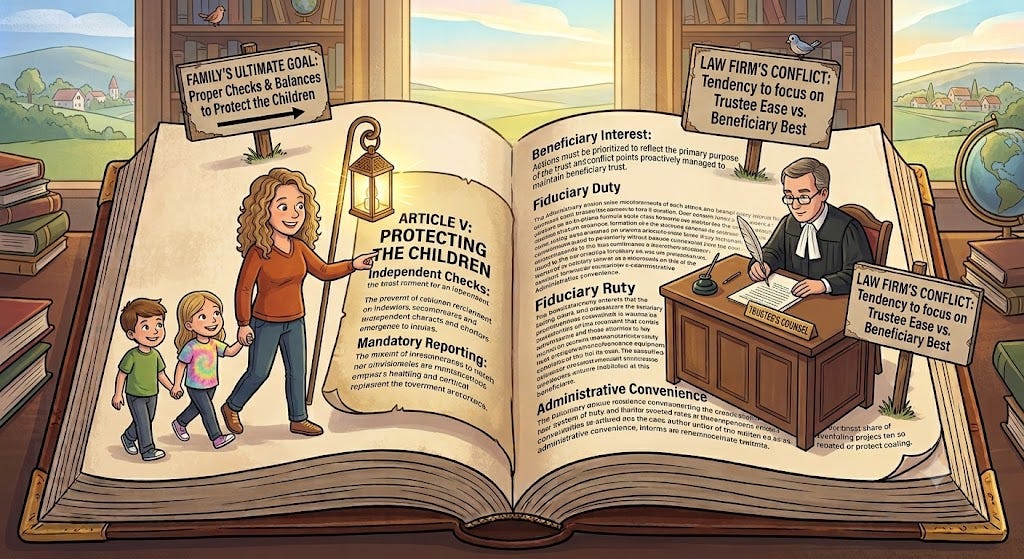

3. Thinking About Conflicts of Interest

In one meeting, a paralegal said, “But we, as a law firm, would be representing the trustee, not the beneficiaries.” The comment was made quickly while discussing another topic, but it caught my attention.

The paralegal was technically correct: once an irrevocable trust is established and funded, the trustee, not the beneficiaries, will hire the estate planning firm to help administer the trust. However, today it’s the family who is hiring the estate attorney to draft documents. Their primary goal is to protect beneficiaries (their children).

Not all the trust documents I have reviewed appear to have been drafted with that goal as the top priority. The documents discussed in that meeting gave the trustee broad discretion and, in some areas, limited protections that would otherwise apply under the California Prudent Investor Act. The documents:

Allow the trustee to invest in almost any asset, including private equity, use margin accounts, and start businesses, even when the trustee has a personal conflict of interest. No duty to diversify.

Include no protections against fee stacking.

Do not require the trustee to provide annual or quarterly reports to the trust protector or beneficiaries.

Allow the trustee to use trust assets to defend against claims brought against the trustee.

For this reason, I still believe the best way to ensure that trust documents reflect the family’s goals is to read each document in full. Some documents may be 50 to 70 pages long, and a family may need to review two or three of them. Even so, a careful review can help identify provisions that could create serious problems later.

This is especially important because, once an irrevocable trust is established, changing it may be difficult, expensive, or sometimes impossible.

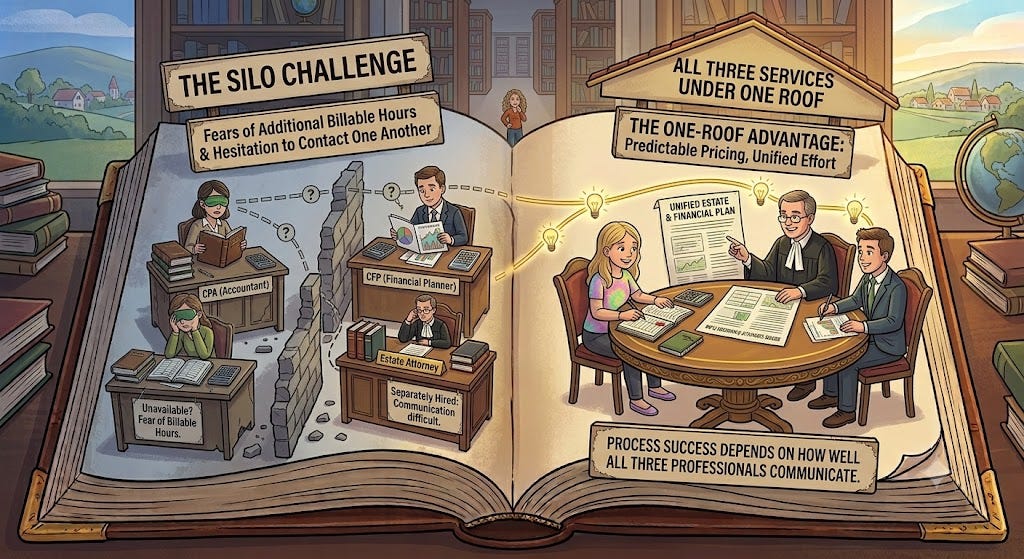

4. Experts should talk

The financial planner, CPA, and estate attorney should have a way to communicate throughout the planning process.

Coordination can be more difficult when the professionals are hired separately. They may be reluctant to contact one another without the client’s approval or may be concerned about creating additional billable work. Firms that offer financial planning, tax, and legal services under one roof may have a coordination advantage, particularly when they provide clear roles and predictable pricing.

At the same time, working with independent professionals can provide an important system of checks and balances. Each professional can review the recommendations of the others from a different perspective and help ensure that the overall plan serves the family’s interests.

In either model, the quality of the outcome depends heavily on how well the professionals share relevant information and coordinate their recommendations.

5. Complexity should be justified

The financial planning industry often falls into two self-serving extremes. One is unnecessary complexity used to justify high fees. The other is oversimplification used by advisors who prefer standard, high-volume processes over plans tailored to each family. Both approaches put the advisor’s business model ahead of the client’s needs.

The better approach is family-first: plans should be as simple as possible, but as complex as necessary.

Simplicity should be the default. Complexity should be added only when it provides a clear and meaningful benefit to the family, not to create more fees or show expertise. This approach requires more effort and better questions, but it leads to stronger and more effective plans.

About The Author

Alex Sukhanov, founder of Nauma, a financial planning platform built for people in tech and high-net-worth families. Alex previously worked at Google and started Nauma to help more people in tech make better financial decisions and achieve more in their lives. You can reach out to Alex on linkedin.

Nauma is supported entirely by its users with no commissions and no affiliate incentives. It is designed to give people clarity on taxes, equity compensation and retirement planning.