The Hidden Risk in “Safe” Investment Portfolios

Understanding duration, rate hikes, and why your bond strategy might not match your timeline.

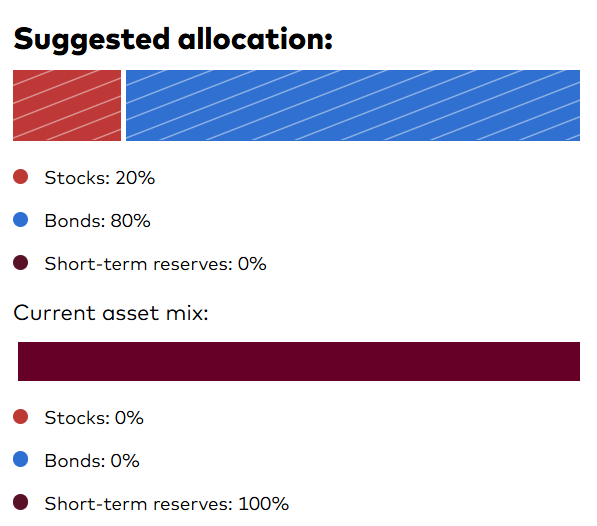

A beginner investor decided to set up a small educational fund in July 2021. They planned to earn an MBA in three years and expected to use the money in 2024. They took a standard Vanguard quiz, which suggested creating a conservative portfolio with 20% stocks and 80% bonds given their timeline.

The investor followed the Boglehead approach and chose low-cost broad-market index funds:

BND - Vanguard Total Bond Market Index Fund

VTI - Vanguard Total Stock Market Index Fund

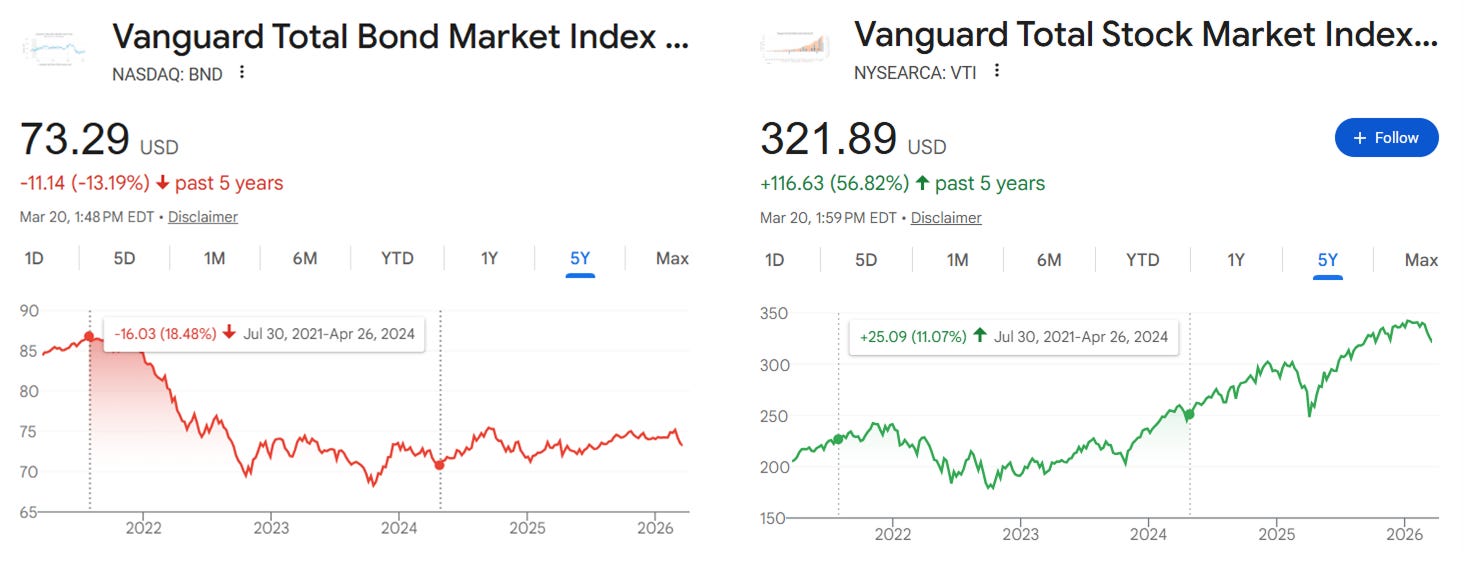

Between July 2021 and April 2024, BND lost 18.48% and VTI gained 11.07%. The conservative portfolio, despite the investor’s attempts to preserve capital, lost 12.57%.

It’s a tough pill to swallow when an investor follows a “conservative” playbook and still ends up in the red. They did everything by the book: low-cost index funds, a Boglehead philosophy, and a high bond allocation to “protect” their capital for a short-term goal. Why did this happen?

Interest Rates and Bonds

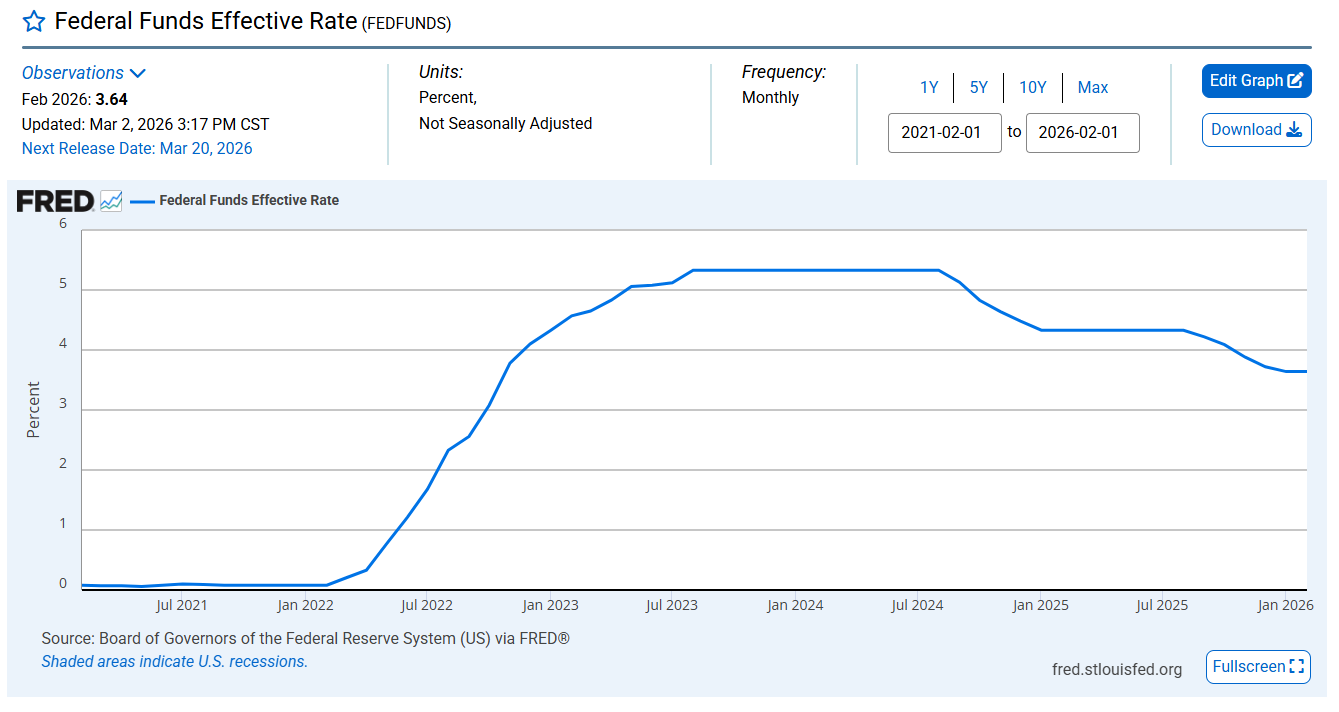

Between 2021 and 2023, the Federal Reserve aggressively raised interest rates to fight inflation. This change broke the inverse correlation between stocks and bonds and created a textbook effect: when interest rates go up, existing bond prices go down.

In July 2021, interest rates were near zero. When the Federal Reserve began aggressively raising rates in 2022, existing bonds (like those in BND) became less valuable because new bonds were being issued with much higher payouts.

This investor fell into a trap that catches many: confusing “conservative” with “risk-free.” While bonds are generally less volatile than stocks, they carry a specific type of risk called interest rate risk, which is measured by a metric called duration.

The duration of a bond fund measures its sensitivity to interest rate changes. A rule of thumb is that for every 1% rise in interest rates, a bond fund will lose value equal to its duration. Because rates rose so quickly and significantly in 2022, BND took a massive hit that its small dividend yield couldn’t offset. In 2021, BND had an average duration of approximately 6.7 years.

6.7 years x 5% rate hike = 33.5% theoretical price drop.

While the interest payments (yields) collected along the way helped offset some of that loss, the sheer speed of the rate hikes led to the worst year for bonds in modern history.

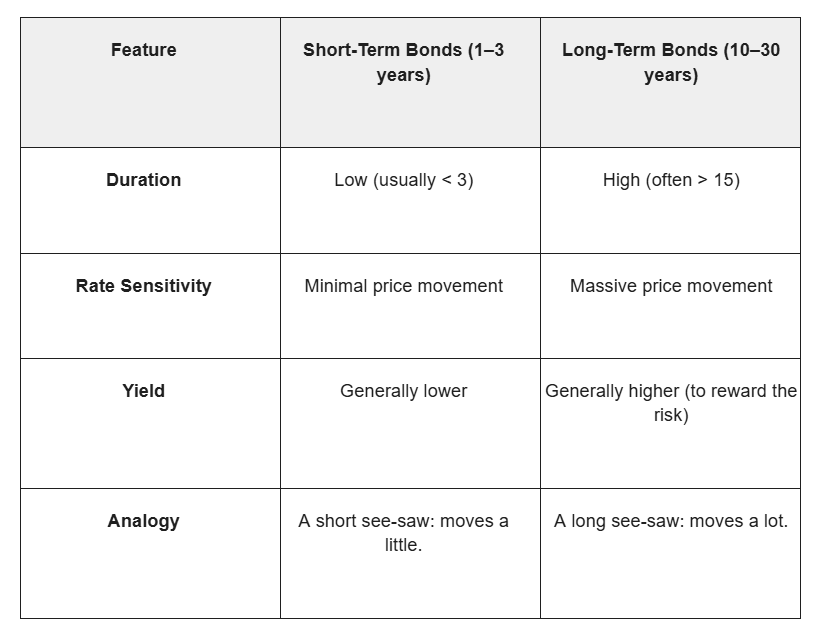

Short-Term vs. Long-Term Bonds

The difference between bond types usually comes down to the trade-off between yield (the paycheck) and volatility (the price swings).

How to Avoid This

The investor’s mistake wasn’t buying bonds; it was buying the wrong duration for their timeline. This is a concept called Liability Matching. If you need the money in three years, you have a “3-year liability.” If you buy a fund like BND with a 7-year duration, you are mismatched. You are taking seven years’ worth of interest rate risk for a three-year goal.

Some options how it can be avoided:

Match Duration to Timeline: If your goal is two years away, your bond duration should be roughly two years. Look for “Short-Term Bond Funds” (like BSV) instead of “Total Market” funds.

Use Defined-Maturity Instruments: For a 2024 goal, the investor could have bought a Certificate of Deposit (CD) or a Treasury Bill that matured in early 2024. This locks in a guaranteed return and eliminates price volatility.

Cash is a Position: For goals less than two years away, High-Yield Savings Accounts (HYSA) or Money Market Funds are often “safer” than bond funds because their duration is effectively zero.

Conclusion

The Vanguard quiz logic relies on a traditional premise: Bonds = Stability and Stocks = Growth. While this is usually true, it assumes a “normal” interest rate environment. What occurred between 2021 and 2024 was an outlier—one of the worst bond markets in decades.

This didn’t happen because the investor did something “wrong.” They followed a standard framework. It happened because interest rates rose faster than expected, and the investor held “total market” bonds with a high duration, making them highly sensitive to those rate hikes.

To avoid this in the future, investors should focus on Liability Matching. By choosing assets that mature exactly when the bills come due—such as T-Bills, CDs, or ultra-short-term bond funds—you remove the guesswork. This ensures that a “conservative” portfolio actually functions as a “protected” one.

I’m Alex Sukhanov, founder of Nauma, a financial planning platform built for people in tech and high-net-worth families. I previously worked at Google. I started Nauma to help people think clearly about complex financial decisions while avoiding hidden incentives, commissions, or generic advice to just invest more.

Nauma is supported entirely by its users with no commissions and no affiliate incentives. It is designed to give people clarity on taxes, equity compensation, retirement, and planning for the future.