Why Financial Goals Should Come Before Investment Strategy

How goal-based planning helps connect wealth to specific life outcomes, reduce stress, and make better long-term decisions

Financial goals are often mentioned in investing and tax discussions, but rarely well defined. For most families, these goals are too vague to actually influence a portfolio or a tax strategy. Unless a family works with a professional financial planner and pays tens of thousands of dollars, their plan and financial goals are likely non-existent.

This creates an unfortunate reality: most people are stuck with cookie-cutter advice and adopt a “more is better” approach: maximizing income and investment returns, without considering the trade-offs.

The problem with chasing “more” is that it eventually buries our purpose. Chasing higher income often translates into doing work that is not aligned with our internal values and often requires doing more of that over time. Higher investment returns come with additional risk and volatility which create stress and ongoing concerns about the markets. By constantly looking for the next peak, we fail to enjoy the present and miss the life we’re working so hard to fund.

Discussing portfolios, tax brackets, or estate planning is meaningless until a family articulates their priorities and both partners are aligned. Defining direction takes time and effort, but gives clarity, lowers stress, and ironically, yields better long-term financial results.

The Failure of the “Single Portfolio”

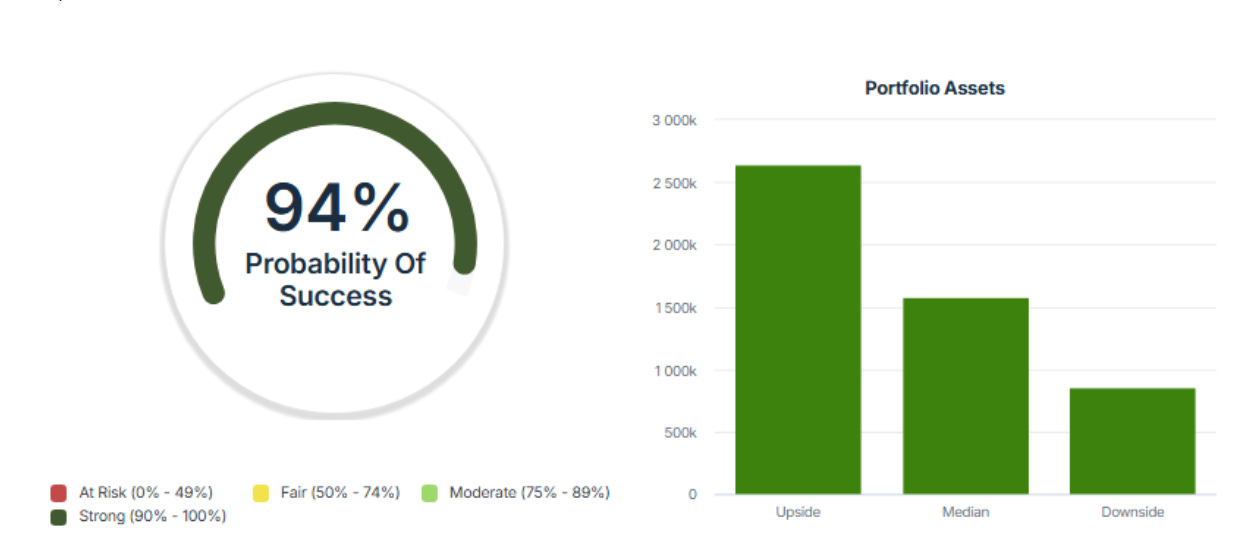

The standard financial planning approach today is the “Single Portfolio”: combining everything together, creating one net worth projection, and running a Monte Carlo simulation for the entire household. This solves the basic question of whether the family has enough, but it ignores the fulfillment problem. The Single Portfolio approach offers little guidance on how to actually use wealth to create a meaningful life while the family still has the health to enjoy it.

It’s hard to tell from a 94% portfolio success rate whether the family can upgrade their house next year, send their kids to a more expensive school in two years, or continuously support a charity they care about. The number does not reveal whether the children are eventually receiving an inheritance aligned with the family’s expectations around generational wealth.

A lack of understanding and uncertainty makes families more conservative. As a result, they stay longer at jobs they no longer need, spend less time with their aging parents, and avoid taking risks such as changing careers or starting their own businesses.

Modern Financial Planning

As prosperity continues to grow, more families are expected to worry less about whether they will have enough money in retirement and more about how to manage their wealth effectively to maximize life experiences. Even today, many families struggle to navigate between under-saving and over-saving, and it is not a trivial problem for most families.

One of the biggest risks facing high-income families today is reaching their 90s with millions of dollars and realizing they could have had more meaningful experiences earlier in life: when they were younger, their loved ones were still around, and they still wanted to do those things.

Separating financial goals helps.

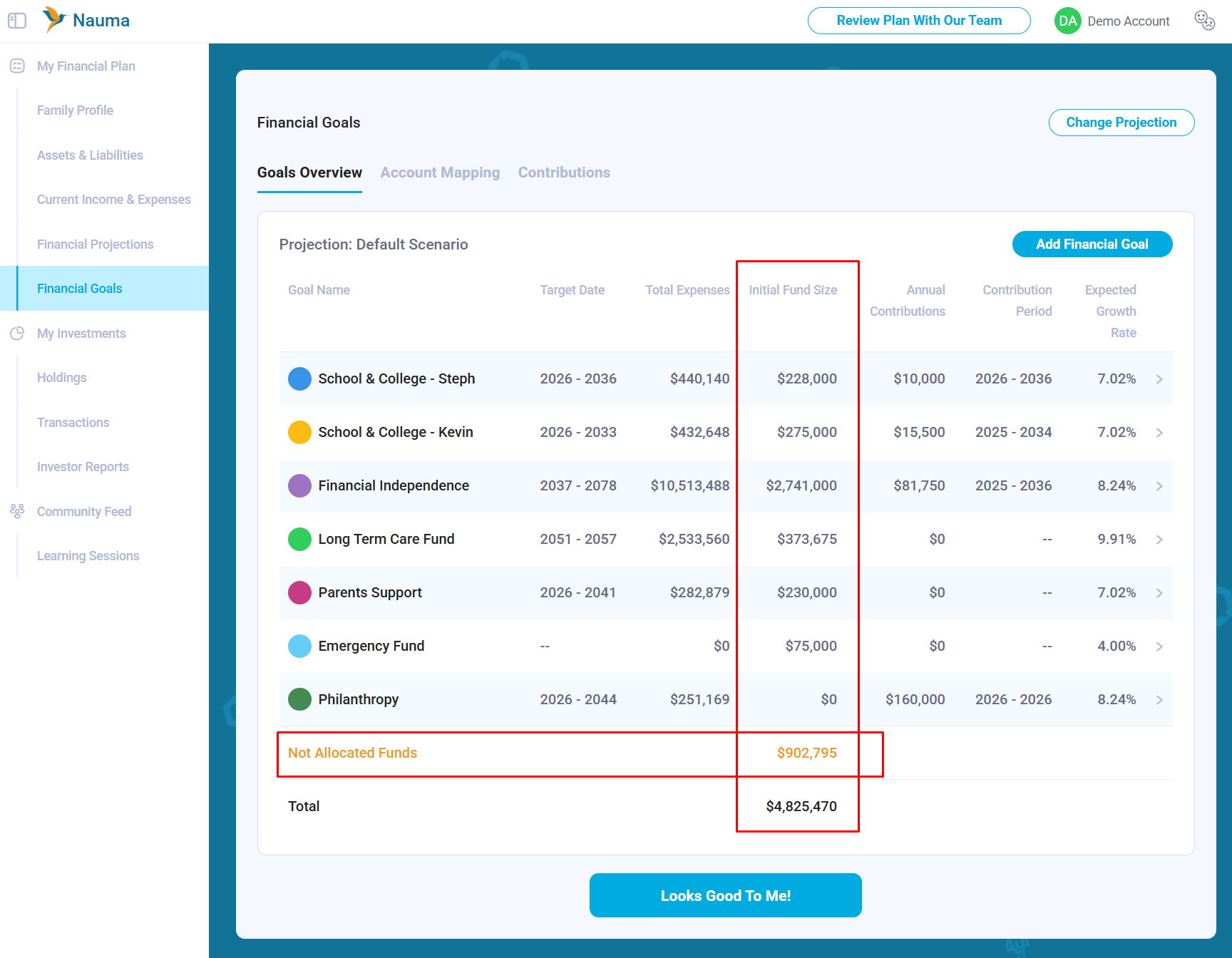

By estimating how much of the family’s current assets should be allocated toward each goal, they can identify their “Not Allocated Funds.” Seeing their “Not Allocated Funds” today helps families realize they can do more. It is often the most powerful insight, more important than any tax optimization or investment strategy that tends to dominate financial conversations.

Aligning Investment Risk & Taxes

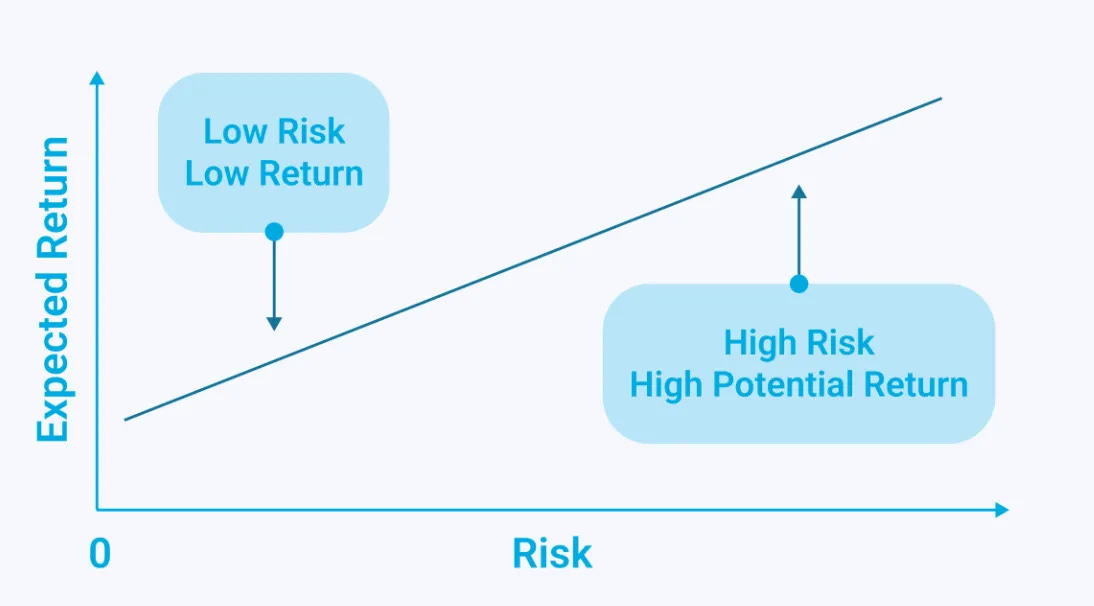

When we treat the entire net worth as a single portfolio, we are forced into a middle-of-the-road risk profile that is often too conservative for long-term legacy goals and too aggressive for short-term needs. This “average” approach creates constant anxiety: a market downturn feels like a threat to next year’s vacation, even though the funds for that vacation should never have been exposed to the S&P 500 in the first place.

By providing tax-advantaged accounts with different tax treatments for specific goals such as retirement, education, healthcare, and charity, the government makes financial planning more complicated. In a “Single Portfolio” framework, it becomes difficult to determine an optimal contribution strategy because some accounts are tax-free while others are tax-deferred. The complexity of the U.S. tax code makes financial planning harder, but separating financial goals reduces this complexity and helps lower the risk of both under-saving and over-saving while taking tax provisioning into account.

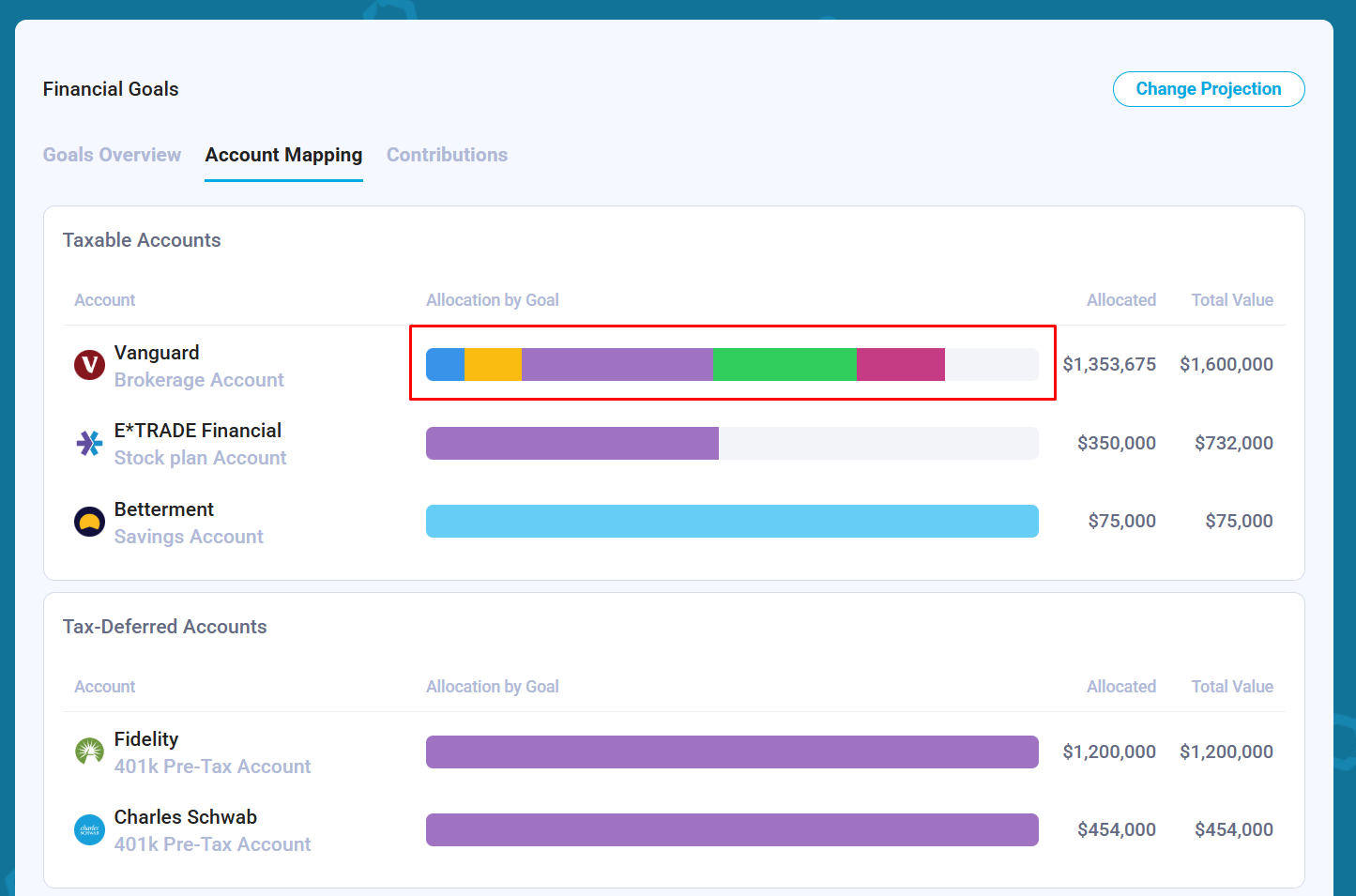

Account Organization

It is impossible to know whether a portfolio is “good” if we do not understand the purpose of the money and when it will be used. Once goals are mapped to specific accounts, families can evaluate whether their portfolio is actually aligned with those goals.

While some people prefer the simplicity of having fewer accounts, the clarity gained from goal-based organization usually far outweighs the administrative burden of managing a few additional accounts.

We are receiving feedback from people who say that organizing their investment accounts by goal has helped reduce stress, especially during major life transitions such as leaving high-paying jobs and becoming households that rely on savings to cover expenses. Having dedicated accounts with clear estimates helped them adopt a “set it and forget it” approach.

Managing an account associated with five different goals, on the other hand, is harder:

Why Goal-Based Planning Is Not Widely Adopted

Despite its benefits, goal-based planning is still not the standard approach for most families.

For DIY investors, the challenge is rarely motivation. Many people genuinely want to make thoughtful decisions about their future, but lack the tools and expertise required to estimate future expenses and construct investment strategies aligned with different goals. Estimating retirement spending, future education costs, healthcare needs, taxes requires a level of planning that most spreadsheets and budgeting apps simply do not provide.

As a result, many investors default to a simple approach: maximizing savings and hoping that “more” will eventually create security. Unfortunately, we do not see this approach working well in practice: people with more than $15M in net worth ask questions very similar to those asked by people with $1M in net worth: “Do I have enough?” Stress does not go away with higher net worth.

The traditional wealth management industry has a different problem: incentives. Most wealth managers operate under the Assets Under Management (AUM) model, where revenue grows as client portfolios grow. This naturally creates a system that rewards asset accumulation and long-term portfolio growth above almost everything else.

Under this model, advising a client to spend more, retire earlier, help their children financially, take a career break, or pursue a lower-paying but more meaningful path can directly reduce the advisor’s future revenue. Even when advisors genuinely care about their clients, the structure itself creates a bias toward preserving and compounding assets indefinitely.

Goal-based planning requires a fundamentally different mindset. Instead of treating wealth accumulation as the final objective, it treats money as a tool designed to support specific outcomes, experiences, and values throughout a family’s life.

About the Author: Alex Sukhanov, founder of Nauma, a financial planning platform built for people in tech and high-net-worth families. Alex previously worked at Google and started Nauma to help more people in tech make better financial decisions and achieve more in their lives. You can reach out to Alex on linkedin.

Nauma is supported entirely by its users with no commissions and no affiliate incentives. It is designed to give people clarity on taxes, equity compensation and retirement planning.